China’s New VAT Rates: Prepare for May 1 Transition

China’s New VAT Rates: Prepare for May 1 Transition

May 15, 2018

China recently declared that it would bring down its value-added tax (VAT) rates and extend the criteria for companies to qualify as small-scale VAT taxpayers, as a major aspect of a RMB 400 billion tax cut package.

In help of this declaration, the State Administration of Taxation (SAT) issued two new circulars explaining the progressions to the VAT system: SAT Announcement [2018] No. 17 and SAT Announcement [2018] No. 18.

The declarations explain changes to the VAT system and timelines and direction for execution. As the main part of the progressions are set to take effect on May 1, 2018, companies situated in or doing business with China should make a move to adjust to the tax updates and decide how their operations will be influenced.

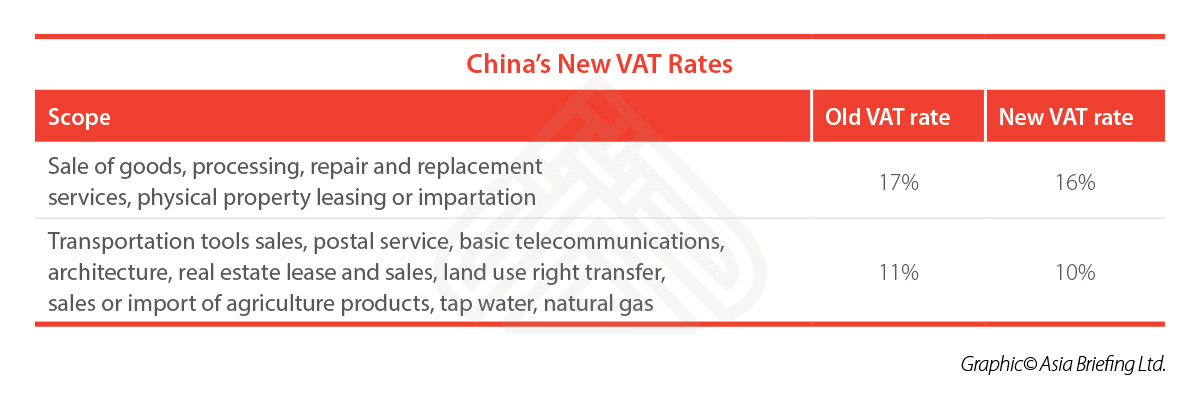

New VAT rates

From May 1, citizens initially subject to VAT rates of 17 percent and 11 percent will now be liable to rates of 16 percent and 10 percent, separately. Taxpayers subject to the six percent VAT rate will see their commitments unaltered.

Additionally, from May 1, export VAT rates and export rebate rates initially subject to 17 percent and 16 percent will be adjusted to 16 percent and 10 percent, individually.

The MOF and SAT determined a progress period for export sales made before July 31, 2018. Specifically:

• For production enterprises: Rebate rates might not be liable to the VAT rate adjustment.

• For foreign trade enterprises: If VAT has been levied at the first VAT rates when purchased, rebate rates should not be liable to the adjustment. If VAT has been required at the adjusted tax rate when bought, the adjusted export tax rebate rate shall be applicable.

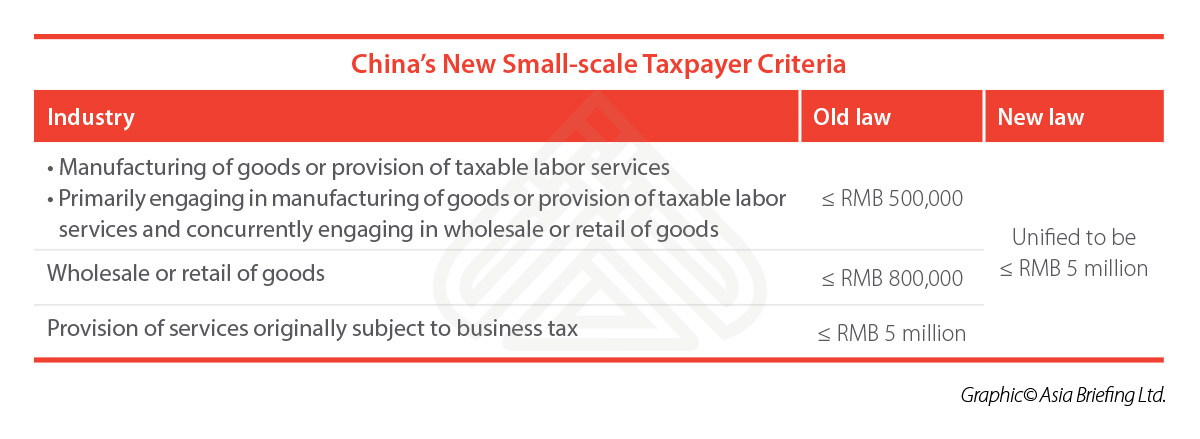

New small-scale VAT taxpayer criteria

Alongside the VAT rate reductions, China will extend the criteria for companies to qualify as small-scale VAT taxpayers, likewise from May 1. Small-scale VAT taxpayers advantage from lower VAT obligations but are for the most part unfit to issue special VAT fapiao.

Beforehand, there were three separate industry-particular tiers to decide small-scale VAT taxpayer status. With the progressions, the three tiers will be unified into a single standard.

Those already registered as general VAT taxpayers have the alternative to transfer to little scale VAT citizen status until December 31, 2018, if they meet the criteria. The criteria to qualify as a small-scale VAT taxpayer depends on a business’ annual revenue. In particular:

Steps for businesses to take

SAT declarations No. 17 and No. 18 describe the treatment of certain VAT-related exercises amid the progress time frame to the new rates.

The declarations elucidate that for exchanges happening before May 1, the original tax rate will be applied for general taxpayers that have not yet issued fapiao but rather should issue one at a later time.

This clarification removes the likelihood for companies to be exposed to tax losses, in situations where goods or services were acquired before the May 1 tax cuts yet the invoices issued a while later, at the lower tax rate.

However, some of the SAT’s explanations stay vague, and it has not yet issued clarifications for the treatment of some other procedures during the transition period.

For example, the strategy for deciding the important VAT for the following points lack guidance when some happen before May 1 and others after May 1:

• The time at which the VAT taxable behavior occurred, which generally refers to goods delivery or confirmation on receipt of goods;

• The time at which point the output VAT is recorded in the accounting books; and

• The time at which the VAT special invoice is issued.

The three points above happen at various circumstances, which confuses the determination of which VAT rate to use for transactions happening during the transition period. If some of the above points start before May 1 yet others happen after, potential tax losses may arise.

As needs be, we prescribe that organizations consider the accompanying practices:

• We encourage companies to contact suppliers frequently. If they are wanting to transfer from general taxpayer status to small-scale taxpayer status, it might affect the company’s VAT rebate.

• For exporting, we encourage companies to guarantee that the exported complete customs clearance and to issue export VAT invoices before July 31, 2018. Inability to do as such may bring about a tax loss from exposure to a lower rebate rate.

• We encourage companies to renew the tax rate settings of their internal systems, for example, the purchase order module and invoice module, to guarantee that the new input VAT rates and output VAT rates are incorporated. We likewise advise companies to educate key users of such changes and perform general checks to ensure the rates are applied correctively.

• We encourage companies to avoid from putting in large orders before the end of April in order to avoid the risks and time commitments related with multi-period transactions.

• The SAT cleared up certain VAT-related issues with announcements No. 17 and No. 18, for example, which rates apply for transactions happening before May 1. Nonetheless, the announcements are not detailed enough to guide tax staff on the best way to operate in practice. We therefore encourage companies to stay in contact with the local tax bureau for further guidance, or to enlist the services of professional tax advisors.

Should you need any further information as regards with “China’s New VAT Rates: Prepare for May 1 Transition”, please do not hesitate to contact our China team at + 86 187 177 31958 or email us at info@opkofinance.com